top of page

M&A outlook points to gradual rebound in deal market in 2024

In brief

The new EY-Parthenon Deal Barometer includes an outlook of recovery for M&A activity in 2024, with US private equity deal volume up 13% and corporate M&A up 12%.

The Deal Barometer leverages the EY-Parthenon Macroeconomics team’s outlook for economic and financial market indicators to predict M&A trends.

Being proactive, rather than waiting for interest rates to fall, appears to be an important strategy for capturing growth opportunities.

The MKC Deal Barometer indicates recovery in the 2024 M&A outlook based on economic and market indicators.

Dealmaking activity has gone through a unique cycle over the past three years. Deal volumes reached historic highs in 2021 and early 2022 driven by a divine combination of moderate inflation, strong economic activity, elevated company earnings and, most importantly, decades-low interest rates.

However, in March 2022, the Federal Reserve embarked on a historic tightening cycle reacting to an environment of persistently elevated inflation. As the cost of capital rapidly surged, slower global economic activity, increased macroeconomic uncertainty and heightened geopolitical tensions led to a severe pullback in dealmaking activity.

In 2023, US private equity (PE) deal volumes are likely to be 27% lower than the peak observed in 2021 and down 19% vs. 2022. US corporate M&A transactions (for deals valued over $100 million) are expected to be down 38% in 2023 compared to the 2021 peak and down 9% relative to 2022.

How MKC can help

We help enable strategic growth through better integrated and operationalized mergers and acquisition…

Looking ahead to the 2024 M&A outlook, EY-Parthenon CEO outlook survey points to renewed CEO enthusiasm for deal activity. Over the next 12 months, the survey found, 52% of US CEOs plan M&A, considerably higher than our global survey, which found only 35% planning deals. In addition, 58% of CEOs plan to divest an asset in that period as leaders seek to fund capital spending in multiple areas.

High on the CEO agenda is forming joint ventures or strategic alliances with third parties (63%) as leaders contemplate lower-risk ways to embrace innovative technologies. Notably, all the CEOs we surveyed are making or planning significant investments in generative AI (GenAI) — with the caveat that many remain uncertain about the direction the technology will take.

This addition features:

New EY-Parthenon Deal Barometer supports CEO M&A optimism

#1

M&A market expected to rebound in 2024

#2

In focus: US private equity deal outlook

#3

In focus: US corporate M&A outlook

#4

Private equity market perspective

#5

1

Chapter 1

New EY-Parthenon Deal Barometer supports CEO M&A optimism

Macroeconomic factors and market indicators point to US M&A rebound in 2024.

Our new EY-Parthenon Deal Barometer indicates that this CEO optimism is well founded, as it points to a gradually rebounding M&A market in 2024. The Deal Barometer uses the EY-Parthenon Macroeconomics team’s outlook for economic and financial market indicators to predict future trends in corporate M&A and PE deal activity. Over the last 35 years, it shows a correlation of 98% between PE deal activity and GDP growth, inflation, corporate profits, and short- and long-run interest rates. The correlation between M&A activity and these economic indicators plus CEO confidence is around 75%, pointing to robust predictive power.

As we enter 2024, the EY-Parthenon Macroeconomics team foresees modest and desynchronized global economic activity with downside risks from elevated geopolitical tensions and tightening financial conditions. Still, the US economy is likely to continue outperforming its peers in terms of GDP growth, with profit margins likely to stabilize and slowly turn higher by the end of 2024. With inflation cooling faster than expected, the Federal Reserve has reached the end of its historic tightening cycle. While officials have embraced a “higher-for-longer” interest rate paradigm, the Fed will very likely proceed with policy rate cuts next year, putting downward pressure on interest rates across the yield curve.

As such, it appears that a proactive strategy of acknowledging and adapting to a higher cost of capital environment will be the most rewarding business strategy. Waiting for rates to fall back to their pre-pandemic levels is bound to be a losing proposition, as it would mean forgoing potential growth opportunities.

The rationale is clear. If scrutinized business decisions make sense in a higher cost of capital environment, they will turn out to be even more profitable when refinanced, as interest rates are more likely to decline than rise over the next three to five years.

Furthermore, companies with generally healthy balance sheets can forgo debt and instead deploy their own capital. Firms that can generate more liquidity and working capital will not only be more resilient but also better able to deploy excess cash to finance M&A activity. Therefore, the higher cost of capital environment should not represent an insurmountable barrier for transactions.

2

Chapter 2

M&A market expected to rebound in 2024

The EY-Parthenon Macroeconomics team sees a soft landing for 2024, with Fed rate cuts likely starting in Q2.

While the EY-Parthenon Macroeconomics team sees a soft landing as the base case for 2024, the odds of a US recession remain around 50%. Hiring restraint and strategic resizing decisions will continue, but we currently don’t anticipate a severe employment pullback. Slower employment and wage growth will constrain disposable income growth, but generally lower inflation, and outright deflation in some goods categories, should support spending. The expectation is for real GDP growth to drift below trend growth through Q2 2024 but then gradually rebound, with real GDP growing a modest 1.4% in 2024.

With the Fed’s favored inflation gauge — core personal consumption expenditures (PCE) inflation — likely falling below 2.5% in the spring, the Fed will likely deliver its first rate cut in Q2 2024. Roughly 75 to 100 basis points (bps) of rate cuts are likely in 2024 and another 150bps in 2025.

Based on the EY-Parthenon Macroeconomics team’s US economic outlook, the EY-Parthenon Deal Barometer estimates US PE deal volumes are likely to rebound 13% in 2024. While this would still leave deal volumes below the 2021 peak, it would represent a faster pace of growth than the average 9% annual pace of growth from 2010 to 2019.

For corporate M&A, the Deal Barometer expects M&A activity to gradually pick up through next year, rising an average of 12% in 2024. We largely anticipate a return to the pre-pandemic levels of activity, with the number of deals in 2024 only about 2% below the average number of deals in 2017–19.

MKC Deal Barometer: forecasting framework

Our framework considers factors such as GDP growth, corporate profits, corporate bond spreads, and changes in short- and long-term interest rates. We also consider CEO confidence¹ as a driver of corporate activity. For our analysis of corporate M&A deals, we focus on deals that are publicly disclosed and have a value of over $100 million.

By using this framework, we can provide business executives with an objective perspective on the volume of US PE and corporate M&A activity in the coming quarters. The EY-Parthenon Macroeconomics team’s deal volume outlooks are informed by three distinct scenarios for the US economy:

Macroeconomic scenario narratives for M&A outlook

Baseline scenario

While signs of economic strength over the summer will likely fuel speculations that the economy is reaccelerating,

we do not expect such strong momentum will be sustained. The recent rapid tightening of financial conditions

spurred by surging bond yields represents a material headwind for business investment and consumer spending.

With myriad headwinds persisting, including tighter credit conditions, the restart of student loan payments,

uncertainty regarding the lagged impact of monetary policy and a fragile global economic backdrop, real GDP growth

is likely to drift below trend for several quarters.

Optimistic scenario

In the optimistic scenario, real GDP growth doesn’t slow much, as the US consumer shows resilience supported

by more robust disposable income growth while businesses turn more optimistic about the outlook, focusing on

long-term investment and hiring decisions. Importantly, stronger supply conditions and rebounding productivity

mean growth is non-inflationary, allowing the Fed to gradually ease monetary policy, supporting some easing in

global financial conditions.

Pessimistic scenario

The pessimistic scenario features an undesirable combination of higher inflation and slower growth — stagflation.

Higher inflation prompted by supply deficiency across multiple sectors, geopolitical fragmentation and rising

commodities prices from global tensions restrain consumer spending. A more hawkish Fed and rapidly tightening

financial conditions lead businesses to retrench with a severe pullback in employment and investment. The economy

heads into a pronounced recession.

3

Chapter 3

In focus: US private equity deal outlook

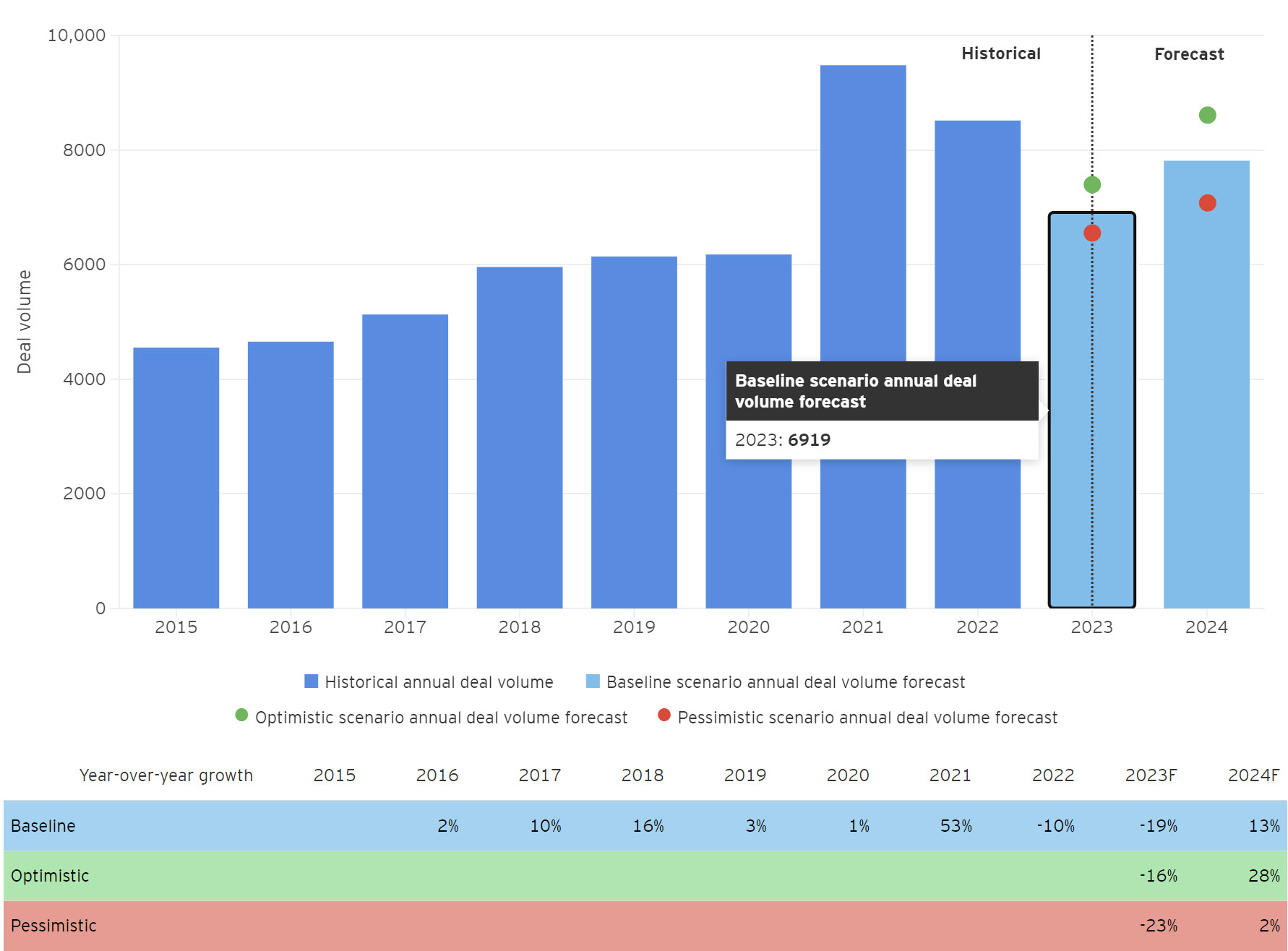

The PE deal volume outlook is up 13% in 2024, surpassing pre-pandemic levels.

The EY-Parthenon Deal Barometer anticipates a gradual recovery in PE M&A activity through 2024 (Figure 1) following a

19% contraction in 2023. It predicts a 13% increase in PE deal volume in 2024, which would still leave deal activity

about 8% below the 2022 level and 18% below the 2021 peak.

While the shortfall relative to recent peaks will be notable, the more important development is that PE deal volume

growth is likely to surpass its pre-pandemic pace next year. Between 2010 and 2019, PE deal volume grew at a 9% compounded

annual growth rate (CAGR).

In our optimistic macroeconomic scenario — where growth is stronger, inflation cooler and interest rates lower — deal

volumes would rise faster in 2024, up 28% year over year (y/y). This would be triple the pre-pandemic pace of growth,

meaning deal volumes would be only 3% below where they would have been absent a COVID-19 crisis.

In our pessimistic macroeconomic scenario — where growth is weaker, inflation hotter and interest rates higher — deal

volumes would rebound with a delay and much less in 2024, showing modest y/y growth of about 2%. In this scenario,

deal volume would trail the 2021 peak by 29%.

US PE deal volume

Our baseline outlook suggests deal volume has found a floor and will finish 2023 ~19% below last year before seeing a

~13% recovery in 2024.

Chart description

Figure 1 illustrates historical US PE deal volume, including quarterly data and annual totals. Historical data is

sourced from Pitchbook and is utilized through Q2 2023. The EY Macroeconomics team’s outlook includes values for the

remainder of 2023 as well as 2024. The baseline forecast for 2023 is deal volumes down 19% relative to 2022. The

optimistic and pessimistic scenarios are -16% and -23%, respectively. The 2024 outlook sees 13% recovery in the baseline.

The optimistic and pessimistic scenarios are 28% and 2% recovery relative to 2023, respectively.

4

Chapter 4

In focus: US corporate M&A outlook

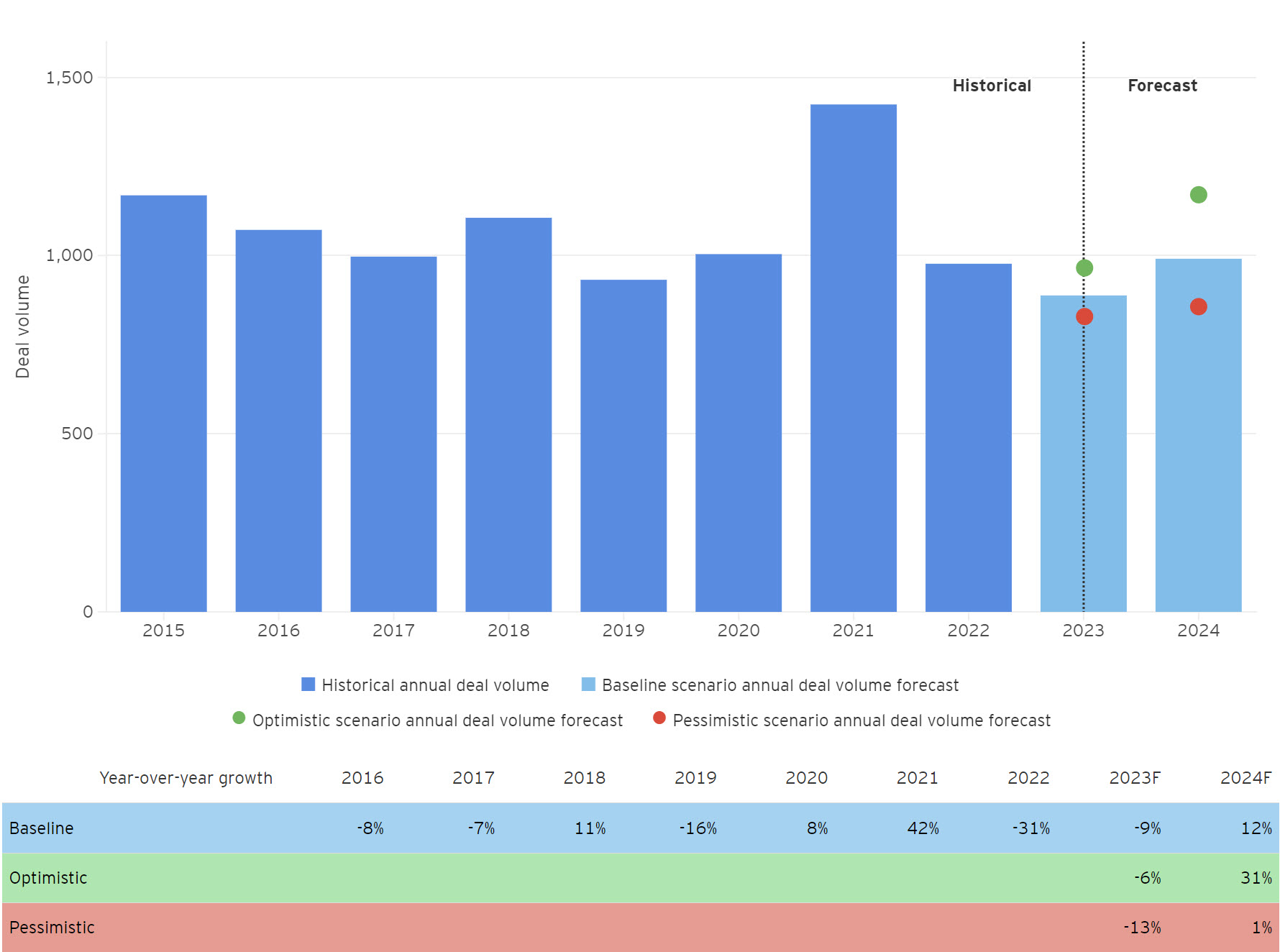

We see M&A activity gradually increasing, reaching 12% gain y/y in 2024.

For corporate M&A, the EY-Parthenon Deal Barometer expects deal volume to gradually pick up through 2024 (Figure 2)

so that deal volume rises 12% y/y, following a 9% decline in 2023. Still, this would be 30% lower than the 2021 peak.

Historically, corporate M&A deal volumes (for deals over $100 million) have been relatively stable around 1,000 deals

per annum. Like the PE deal space, the pandemic resulted in a large positive shock for deal volumes, registering an

impressive jump of more than 40% in 2021. The Deal Barometer largely anticipates a return to the pre-pandemic levels of

activity, with the number of deals in 2024 only about 2% below the average number of deals in 2017–19.

In our optimistic scenario, our Deal Barometer anticipates more forceful recovery for 2024, with the total number of

deals increasing 31%. In the downside scenario, M&A activity is expected to show a muted recovery with only 1% growth in 2024.

US corporate M&A deal volume

Our baseline outlook suggests corporate deal volume will finish 2023 ~9% below last year before seeing a ~12% recovery in 2024.

Chart description

Figure 2 illustrates historical US corporate M&A deal volume (>$100m value, publicly disclosed), including quarterly

data and annual totals. Historical data is utilized through Q2 2023. The EY-Parthenon Macroeconomics team’s outlook

includes values for the remainder of 2023 as well as 2024. The baseline forecast for 2023 is deal volumes down 9% relative

to 2022. The optimistic and pessimistic scenarios are -6% and -13%, respectively. The 2024 outlook sees 12% recovery in the

baseline. The optimistic and pessimistic scenarios are 31% and 1% recovery relative to 2023, respectively.

5

Chapter 5

Private equity market perspective

Deal types are expanding, with carve-outs increasing.

Today’s

PE market

is seeing a broader array of deal types, in contrast to the first half of this year, which

was characterized by a very narrow focus on take-privates and add-on transactions. Recent months, for example,

have seen several large carve-outs from corporate parents seeking to divest non-core or orphan assets.

Of the top 20 deals announced in Q3, approximately one-third were carve-outs, with an aggregate value of nearly

US$25b (in contrast, Q1 was just 5% carve-outs). For PE firms — especially the largest funds — these deals can be

competitive differentiators, providing opportunities for firms to leverage their scale and their operational

expertise to drive value.

Exit markets have shown similar signs of recovery in recent months, albeit at a slightly slower pace than

acquisitions. In the third quarter of this year, PE firms announced 68 exits via M&A, up from 47 in the first

quarter of the year and up from 57 in Q2.

From a sector perspective, technology continues to be a key area of focus, accounting for nearly one-third of PE

activity by value over the last 12 months, up from 26% over the preceding 12 months. Investors remain attracted

to the industry’s long-term secular growth story, its relative resilience in the face of macro headwinds and the

growing integration of technology in sectors such as health care, finance, industrials and energy.

Over the last 12 months, the health care sector has accounted for 10% of PE investment by value, up from just 6%

over the preceding 12 months — that focus is expected to accelerate.

For firms’ existing portfolios of assets, one of the primary consequences of extended hold periods is imperative

to optimize operational value-add to offset longer ownership periods. Even for new acquisitions, with many assets

continuing to be “priced to perfection,” there is little wiggle room for suboptimal execution.

Footnotes

- MarCaps, LLC. Proprietary research on Winning Marketing Organizations (WMOs).

Summary

The new EY-Parthenon Deal Barometer indicates a rebound in US M&A activity in 2024, with volumes returning near pre-pandemic levels. The barometer incorporates the EY-Parthenon Macroeconomics team’s outlook for economic and financial market indicators to predict M&A trends.

0

6

Enhance risk and compliance oversight

Future-fit boards embrace risk and seize the upside.

HTML goes here

Related articles

M&A activity in 2024 driven by new technology, consolidation and PE. Tech, energy and life sciences bear watching.

12 Dec 2023 | Elizabeth Kaske

A robust strategy can bring value to both buyers and sellers throughout the M&A lifecycle.

08 Aug 2023 | Frederic Veron

Mega mergers can pay off with higher shareholder value if companies take the right approach.

26 Jul 2023 | Elizabeth Kaske

Contact us

Connect with our experts. We will help you achieve much more.

bottom of page